Calculation of Compensation – No. 4 Guidance concerning the calculation of different types of variable pay

1. Purpose

This Interpretation, Policy and Guideline (IPG) provides guidance on how to:

- Identify and define different types of variable pay; and,

- Calculate different types of variable pay.

This IPG is the fourth in a series that addresses the calculation of compensation. The other IPGs in this series are:

- No. 1: Guidance Concerning the Definition of Compensation.

- No. 2: Exclusions.

- No. 3: An Interpretation of Salary and Determining the Highest Salary Rate.

- No. 5: Guidance Concerning the Calculation of Different Types of Incentive Pay.

- No. 6: Guidance Concerning the Calculation of Indirect Compensation Elements.

This document does not replace expert legal and/or compensation advice. This document is technical in nature and should not be used as a plain language resource. Plain language resources are available at https://www.payequitychrc.ca/en.

The term employer in this document can also refer to a group of employers that has been recognized by the Pay Equity Commissioner.i

2. Definition of compensation

Section 3(1) of the Pay Equity Act defines compensation as any form of remuneration payable for work performed by an employee and includes:

- Salaries, commissions, vacation pay, severance pay and bonuses;

- Payments in kind;

- Employer contributions to pension funds or plans, long-term disability plans and all forms of health insurance plans; and,

- Any other advantage received directly or indirectly from the employer.

For more information, see Calculation of Compensation – No. 1: Guidance Concerning the Definition of Compensation on the pay equity publications web page: https://www.payequitychrc.ca/en/publications.

3. Guidance on different types of variable pay

The following sections provide guidance on how to define and calculate different types of variable pay when determining the total compensation of a job class.

3.1. Identifying variable pay

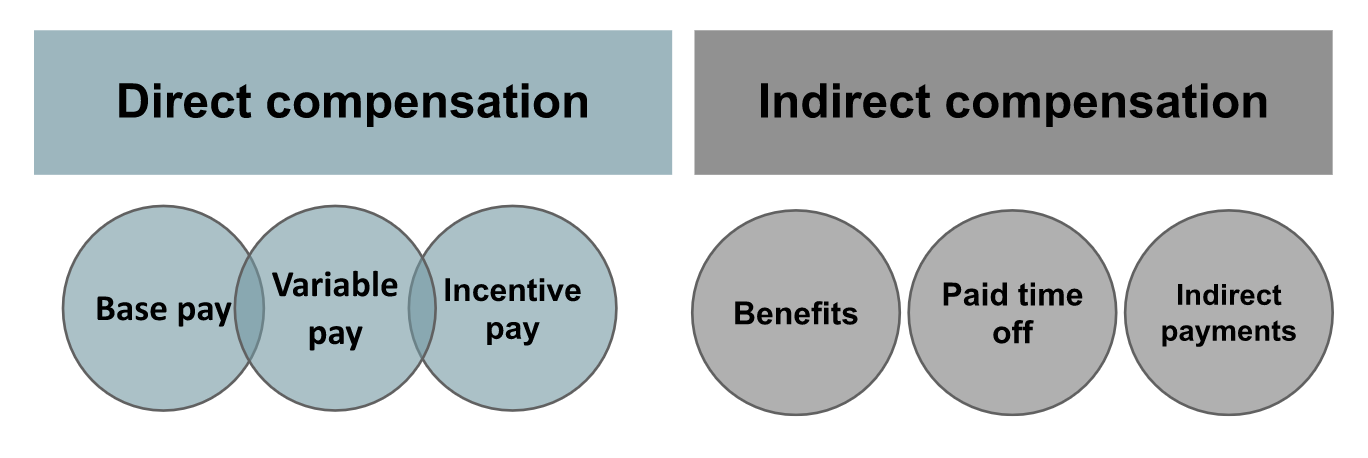

Variable pay is identified as a direct compensation element in the total compensation model.

Direct compensation includes:

- Base pay;

- Variable pay; and,

- Incentive pay.

Indirect compensation includes:

- Benefits;

- Paid time off; and,

- Indirect payments.

Variable pay is typically volume based. Examples include:

- Piecework rates and/or per kilometre rates.

- Tips; and,

- Commissions.

Variable pay includes payments an employee receives for meeting prescribed volume-based or output productivity—for example, distance driven or production unit volumes. It includes elements such as piecework rates, per kilometre rates, tips and commissions.

Variable pay can also include performance-based or incentive program amounts based on prescribed performance management programs— for example, defined short-term and long-term incentive plans.

For the purposes of this Interpretation, Policy and Guideline, variable (performance-based) incentive compensation is excluded. For more information on incentive-based compensation, see Calculation of Compensation – No. 5: Guidance Concerning the Calculation of Different Types of Incentive Pay on the pay equity publications web page: https://www.payequitychrc.ca/en/publications.

3.2. Calculating different types of variable pay

Variable pay is used differently in federally regulated workplaces across Canada. Some organizations use compensation structures that:

- Have fixed or predictable variable pay elements. In these cases, the employer or pay equity committee may calculate the average, median or target rate for the job class as base pay. These calculations should reflect how much an employee who is meeting target levels of output can realistically earn.

- Have variable pay amounts that are not fixed or predictable. In these cases, the employer or pay equity committee may choose to use “0” as base pay and use the average, median or target rate to calculate the amount to include in total compensation.

- Have variable pay amounts that are provided in addition to base pay that are at risk and unpredictable (for example, exceeding above-target performance in a defined incentive or outcomes-based reward program). In these cases, these amounts may be calculated as incentive pay.

For more information, see Calculation of Compensation – No. 5: Guidance Concerning the Calculation of Different Types of Incentive Pay on the pay equity publications web page: https://www.payequitychrc.ca/en/publications.

To avoid fluctuations associated with variable types of pay, it may be helpful to analyze earnings over a longer period of time.ii Given the reality of economic cycles and the related impact on variable operational results, variable pay practices, for example, may need to be examined on a rolling three-year average basis.

3.2.1. Piecework rates and per kilometre rates

Piecework rates are a form of compensation whereby workers are paid by the unit produced rather than being paid on the basis of time spent on the job.iii An example is per kilometre rates, where an employee is paid a predetermined or fixed rate for each kilometre driven.

Example: Fixed or predictable variable pay as base pay

Scenario: A trucking company puts all of its long-haul truck drivers into one job class. For these drivers, base pay is determined and paid in the form of per kilometre rates.

The company compensates its drivers at a rate of $0.45 per kilometre.

Each driver puts in no more than 10 hours of driving time per day and works five days per week, 52 weeks per year.

Calculation: For pay equity, the employer or pay equity committee chooses to calculate the average rate for the job class.

| Job position | Kilometres per year | Annual amount ($) | Hourly amount ($/hour) |

|---|---|---|---|

| 1 | 143,000 | 64,350 | 24.75 |

| 2 | 140,000 | 63,000 | 24.23 |

| 3 | 136,000 | 61,200 | 23.54 |

| 4 | 130,000 | 58,500 | 22.50 |

Average hourly amount = ($24.75 + $24.23 + $23.54 + $22.50) ÷ 4 = $23.76

Conclusion: For the purposes of pay equity, the employer or pay equity committee would use the average hourly amount of $23.76 as base pay for the job class.

3.2.2. Commissions

A commission-based compensation structure compensates individuals based on predetermined outcomes, such as sales revenue, gross or profit margin and client retention. In most cases, a commission is an amount paid to an employee for making a business transaction (for example, a sale) or performing a predefined service.

Example: Variable pay amounts that are not fixed or predictable.

Scenario: A bank has a financial planning job class. The positions in this job class are all part of the same 100% commission and bonus-based compensation plan. All amounts received are based on performance.

Calculation: For pay equity purposes, the employer or pay equity committee chooses to use “0” as the base pay and variable pay amounts, as the compensation plan is 100% based on performance. Variable pay amounts are not fixed or predictable.

| Monthly gross performance | Commission grid |

|---|---|

| First $10,000 of monthly gross | 25% |

| All gross above $10,000 | 50% |

Conclusion: For the purposes of pay equity, the employer or pay equity committee may use “0” as base pay. Amounts that meet target are included in the calculation of total compensation, while those amounts that exceed target may be excluded, should they meet the criteria outlined in section 46 of the Pay Equity Act.

Example: Variable pay as incentive pay

Scenario: Telecommunications sales representative job class

Alex is a telecommunications sales representative and is paid commissions in addition to base pay of $40,000 per year. The company set Alex’s target for the year at $50,000 of new revenue. This agreement was documented, and the sales plan and expectations were clearly articulated.

Tier 1 of the plan represents $0 to $50,000 in revenue, with a 5% commission rate (target). Tier 2 of the plan represents $50,001 to $70,000, with an 8% commission rate for exceeding target rates.

Alex managed to exceed his target by $10,000 by generating $60,000 in revenue.

Incentive calculation: For pay equity purposes, the employer or pay equity committee would multiply the earned commission amount at target as follows:

$50,000 × 0.05 = $2,500 at target rate

Based on a 40-hour workweek, this equates to $1.20 per hour.

For pay equity, the employer or pay equity committee would multiply the earned commission above target as follows:

($60,000 − $50,000) × 0.08 = $10,000 × 0.08 = $800 above target rate

Based on a 40-hour workweek, this equates to $0.38/hour paid for exceeding the target sales plan.

Conclusion: For the purposes of pay equity, the employer or pay equity committee would include $1.20/hour in the calculation of total compensation as variable pay and $0.38/hour as incentive pay for the job class should the merit-based compensation plan not meet the section 46 criteria outlined in the Pay Equity Act.

4. Referenced Pay Equity Act provisions

3(1)

compensation means any form of remuneration payable for work performed by an employee and includes

- salaries, commissions, vacation pay, severance pay and bonuses;

- payments in kind;

- employer contributions to pension funds or plans, long-term disability plans and all forms of health insurance plans; and

- any other advantage received directly or indirectly from the employer. (rémunération)

Calculation

44 (1) An employer — or, if a pay equity committee has been established, that committee — must calculate the compensation, expressed in dollars per hour, associated with each job class for which it has determined, under section 41, the value of the work performed.

Group of job classes

(2) If an employer or pay equity committee, as the case may be, treats a group of job classes as a predominantly female job class in accordance with section 38, the compensation associated with that job class is considered to be the compensation associated with the individual predominantly female job class within the group that has the greatest number of employees.

Salary

(3) For the purpose of determining salary in the calculation of the compensation associated with a job class, the salary at the highest rate in the range of salary rates for positions in the job class is to be used.

Exclusions from compensation

45 An employer — or, if a pay equity committee has been established, that committee — may exclude from the calculation of compensation, with respect to each job class in respect of which compensation is required to be calculated, any form of compensation that is equally available, and provided without discrimination on the basis of gender, in respect of all of those job classes.

Differences in compensation excluded

46 An employer — or, if a pay equity committee has been established, that committee — must exclude from the calculation of compensation associated with a job class any differences in compensation that either increase or decrease compensation in any or all positions in that job class as compared with the compensation that would otherwise be associated with the position, if the differences are based on any one or more of the following factors and those factors have been designed and are applied so as not to discriminate on the basis of gender:

- the existence of a system of compensation that is based on seniority or length of service;

- the practice of temporarily maintaining an employee’s compensation following their reclassification or demotion to a position that has a lower rate of compensation until the rate of compensation for the position is equivalent to or greater than the rate of compensation payable to the employee immediately before the reclassification or demotion;

- a shortage of skilled workers that causes an employer to temporarily increase compensation due to its difficulty in recruiting or retaining employees with the requisite skills for positions in a job class;

- the geographic area in which an employee works;

- the fact that an employee is in an employee development or training program and receives compensation at a rate different than that of an employee doing the same work in a position outside the program;

- the non-receipt of compensation — in the form of benefits that have a monetary value — due to the temporary, casual or seasonal nature of a position;

- the existence of a merit-based compensation plan that is based on a system of formal performance ratings and that has been brought to the attention of the employees; or

- the provision of compensation for extra-duty services, including compensation for overtime, shift work, being on call, being called back to work and working or travelling on a day that is not a working day.